The yield curve is flattening like a pancake.

Tightening cycles tend to do that.

Furthermore, the effective float of 10-year and longer U.S. notes and bonds is relatively small and greatly distorts the bond market signal. We have written about this several times.

Given the small float of tradeable Treasury notes and bonds, the market is subject to massive short squeezes if it gets too offside and rapid ramps if traders algos try and game duration. Information Positive Feedback LoopMany in the market, we fear, are being hoodwinked by the flattening yield curve, however. It’s purely the result of technicals and not economic fundamentals. Nevertheless, some still look to the badly distorted bond market as a signal of the health of the economy and act accordingly. Such as delaying capital spending; becoming more risk averse; and cutting back on consumption, for example. A flatter yeld curve also makes bank lending less profitable. This could thus lead to what George Soros calls “reflexivity” where the negative, but false, signal from the bond market actually causes an economic slowdown or leads to a recession. So much for efficient markets. Recall the famous line of one prominent market strategist during the dark days of the great recession,

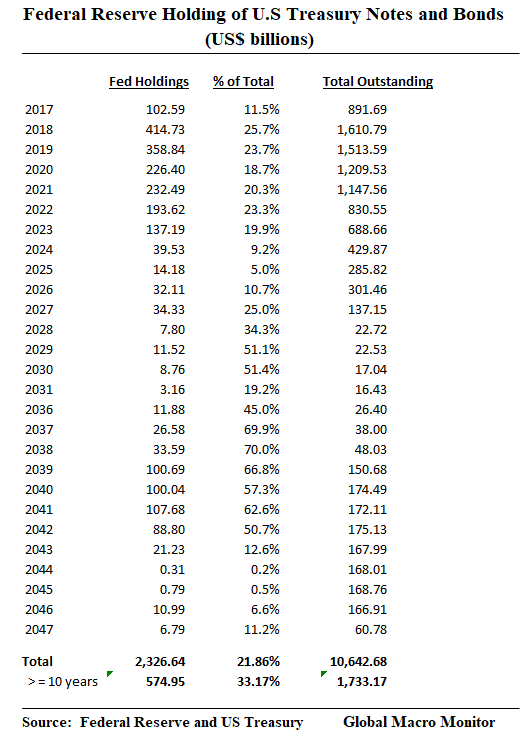

Or the ubiquitous, “what is the bond market telling us?” Come on, man! The Fed Needs To Start Selling Longer Dated SecuritiesIt would, therefore, behoove the Fed to sell some of its longer dated Treasury holdings to steepen the yield curve. The follwing table shows the Federal Reserve’s holdings of U.S. Treasury securites and the total Treasury outstandings for each year. This table does not include T-Bills. If the Fed were to just let its balance sheet “run off” — that is not rollover maturing notes and bonds — it would cause additional pressure on short-term interest rates even as policy rates are rising. It could also potentially invert or further disort the front-end of the yield curve and destablize the money markets. Looking at the data in 2018 and 2019 large maturities are coming due. Rolling a portion of these maturities and selling longer-dated securities would probably cause less disruption in the market and be a more optimal strategy of reducing the Fed balance sheet.

Announcement EffectJust announcing the fact the Fed was contemplating such a strategy of unloading longer dated Treasuries first would cause the yield curve to steepen. The market would begin to front run the Fed. Bill Gross & Co. would kick into action and “sell what the Fed wants to sell.” And because there are so relatively few Treasuries outstanding with maturities longer than 10-years, it is unlikely it would cause a bond market debacle, which many believe is coming. The total stock of Treasury securities with maturities longer than 10-years is smaller than the combined market capitalization of just Apple, Google, and Amazon, for example. If bonds become too oversold, the Fed could easily engineer a short squeeze to bring the yield curve back to where it desires. Recall, the Fed losing control of the yield curve prior to the financial crisis to foreign central banks recyling capital flows back into the U.S. is what Alan Greenspan singles out as the major cause of the housing bubble. The Fed moved the funds rate up 425 bps and the 10-year and mortgage rates barely budged.

RisksThe risk is that foreigners begin to sell. But where will they go? Spanish 10-years at 1.43 percent? German 10-year bunds at 0.266 percent? How about a 10-year Japanese JGB at 0.067 percent? In fact, low foreign yields and the ensuing portfolio effect is keeping the U.S. 10-year note well anchored below 2.60 percent and another factor distorting the yield curve. Credit and Equity MarketsThat is where there we could have some short-term problems and overshooting. But our sense, many are waiting to pounce on a sell-off in the spread and equity markets. Too many pensions are underfunded and too many seniors are yield strarved. Having some dry powder makes sense. It’s coming and you will have to act fast. ConclusionA sustained spike in inflation? Tilt! Game over, comrades. from http://capitalisthq.com/reflexivity-and-why-the-fed-must-sell-the-long-end/

0 Comments

Leave a Reply. |

ABOUT USUncensored News on Markets, Politics, Trump News - CapitalistHQ.com- Most Influential Financial, Economics & Political Website with Crisp Commentary from Political and Business Insiders, Trump News, Zerohedge and Market Gurus. Archives

December 2017

Categories |

RSS Feed

RSS Feed